Buying a home is often the biggest financial milestone in an individual’s life. In a bustling, high-growth market like Hyderabad, where property prices in prime corridors like Kondapur and Hitec City are appreciating rapidly, the financial load of buying a premium home can be heavy for a single earner.

This is where Joint Home Ownership steps in as a game-changer.

Joint home ownership allows two or more individuals (usually spouses or family members) to own a property together, offering significant financial and legal advantages:

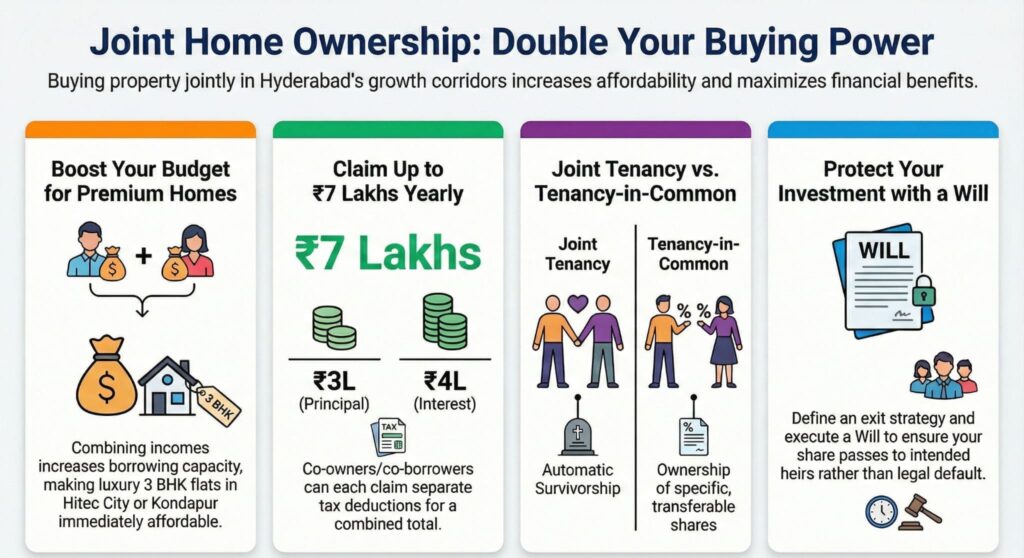

- Enhanced Loan Eligibility: Combining incomes increases your borrowing capacity, making premium 3 BHK flats in Hyderabad more affordable.

- Double Tax Benefits: Co-owners who are also co-borrowers can separately claim tax deductions up to ₹3.5 Lakhs each (₹2L interest + ₹1.5L principal) per financial year.

- Succession Planning: Ownership structures like “Joint Tenancy” ensure seamless transfer of rights to the surviving owner, while “Tenancy-in-Common” allows distinct shares to be passed to heirs.

Whether you are a young couple eyeing spacious 3 BHK flats in Hyderabad or a family investing in luxury apartments, buying a property jointly isn’t just about sharing a roof—it’s about sharing the financial burden, multiplying tax savings, and securing your family’s future. However, navigating the legal labyrinth of co-ownership requires due diligence. From understanding the difference between “Joint Tenancy” and “Tenancy-in-Common” to mapping out exit strategies in case of disputes, being informed is your best defense.

This guide breaks down everything Hyderabad homebuyers need to know about owning property together in 2026.

What We’re Seeing: Joint Ownership Trends in Hyderabad

In the past two years, roughly 35-40% of the property registrations our team has handled in West Hyderabad involve joint ownership — predominantly husband-wife combinations, followed by parent-child structures. The driving factor isn’t just tax optimization; it’s the practical reality that Hyderabad’s premium micro-markets now price 3BHK apartments at ₹1-1.5 Cr, making dual-income eligibility essential for home loan approval.

One pattern we’ve noticed at the Sub-Registrar offices in Banjara Hills and Madhapur: documentation errors in joint ownership deeds are the single biggest reason for registration delays. The most common mistake is mismatched shares between the sale deed and the home loan agreement — for example, the deed says 50:50 ownership but the loan is entirely in one person’s name. We always advise our buyers to align these documents before the registration appointment, which typically saves 2-3 weeks of back-and-forth.

— Auro Realty Team | Source: IGRS Telangana, RERA Telangana

Types of Joint Ownership Structures in India

When you sign that sale deed, you aren’t just buying a home; you are defining a legal relationship. In India, joint ownership typically falls into two categories, and choosing the wrong one can lead to severe inheritance complications later.

A. Joint Tenancy (Right of Survivorship)

This is the most common structure for married couples.

- The Rule: In Joint Tenancy, the concept of “Right of Survivorship” applies. If one co-owner passes away, their share automatically transfers to the surviving co-owner, regardless of what a Will might say.

- Ownership Share: Usually, this implies a 50-50 ownership split, though the deed should explicitly state this.

- Best For: Spouses who want to ensure the surviving partner inherits the home without legal hassles.

B. Tenancy-in-Common

This is often preferred by siblings, business partners, or friends buying investment properties together.

- The Rule: Each co-owner holds a specific, distinct share of the property (e.g., Owner A holds 60%, Owner B holds 40%).

- Inheritance: Upon the death of one owner, their share does not go to the other co-owner. Instead, it passes to the deceased owner’s legal heirs as per their Will or succession laws.

- Best For: Investors pooling money for flats for sale in Kondapur or siblings who want to leave their share to their own children.

Pro Tip: Your sale deed must explicitly state the type of ownership. If the deed is silent, Indian courts typically presume “Tenancy-in-Common,” which can be disastrous for a surviving spouse if other legal heirs stake a claim.

What We’ve Observed in Practice

In our experience facilitating joint ownership transactions across Hyderabad, roughly 60% of co-ownership deals involve married couples, 25% are parent-child combinations (typically for tax planning), and 15% involve siblings pooling resources. The most common friction point we’ve seen isn’t legal — it’s the exit strategy. Couples rarely plan for what happens if one party wants to sell. We now strongly recommend that all joint buyers execute a co-ownership agreement specifying sale triggers, buyout terms, and dispute resolution before completing registration at the Sub-Registrar’s office.

— Auro Realty Team | Our Editorial Standards

Home Loan Eligibility & EMI Sharing for Co-Owners

One of the primary triggers for joint ownership is the ability to afford a better home. If you have your heart set on luxury apartments in West Hyderabad but your individual salary only qualifies you for a budget home, a joint loan bridges that gap.

Boosting Loan Eligibility

When you apply for a home loan with a co-applicant (spouse, parent, or sibling), the bank considers your combined income.

- Example: If your salary qualifies you for a ₹50 Lakh loan, and your spouse qualifies for ₹40 Lakhs, together you can secure a loan of ₹90 Lakhs.

- Result: This allows you to upgrade from a compact 2 BHK to expansive 3 BHK flats in Hyderabad prime locations immediately, rather than waiting years to save up.

Structuring the EMI Burden

While the bank holds both applicants equally liable for repayment, you can decide how to split the EMI servicing internally.

- Income Ratio Split: Many couples split the EMI in proportion to their salaries (e.g., 60:40). This helps in maximizing tax benefits for the higher earner (more on this below).

- Bank’s Perspective: Remember, even if you agree to pay 50% each, if one defaults, the bank will come after the other for the full outstanding amount.

Tax Benefits Available to Each Co-Owner

This is the financial “sweet spot” of joint ownership. Under the Income Tax Act, tax benefits are not capped per property, but per owner—provided they are also co-borrowers.

Double the Deduction

If you and your spouse are co-owners and co-borrowers, you can both claim deductions separately:

- Principal Repayment (Section 80C): Each can claim up to ₹1.5 Lakhs.

- Combined Benefit: ₹3 Lakhs.

- Interest Payment (Section 24b): Each can claim up to ₹2 Lakhs (for self-occupied property).

- Combined Benefit: ₹4 Lakhs.

The ₹7 Lakh Advantage

For a high-value property—say, one of the premium flats for sale in Kondapur costing ₹1.5 Cr—the annual interest burden in the initial years will easily exceed ₹8-9 Lakhs. A single applicant would max out their ₹2 Lakh limit and lose the rest.

- Jointly: A couple can claim a total of ₹7 Lakhs (₹3L Principal + ₹4L Interest) in deductions annually, significantly reducing the household tax liability.

Crucial Requirement: To claim these benefits, you must be a Co-Owner of the property AND a Co-Borrower on the loan. Being just a “loan guarantor” or just a “name on the deed” without paying EMIs disqualifies you from tax breaks.

Legal Risks, Exit Clauses & Dispute Scenarios

Joint ownership is fantastic when relationships are smooth, but real estate assets are illiquid, making disputes messy. What happens in the case of divorce, estrangement, or insolvency?

The “Exit Strategy” Clause

Before registering the property, co-owners (especially non-spouses) should have a legal agreement outlining an exit strategy.

- Right of First Refusal: If one owner wants to sell, they must offer their share to the other co-owner first before going to a third party.

- Buyout Formula: How will the property be valued if one wants to buy the other out? Agreeing on using a certified market valuer prevents pricing wars later.

Divorce and Property

In a divorce settlement, the property usually has to be sold to split the proceeds, or one spouse buys out the other’s share.

- The Loan Trap: Even if the court grants the property to one spouse, the bank still considers both liable for the loan until it is refinanced or closed. You must ensure the exiting spouse’s name is formally removed from the loan records by the bank.

Inheritance, Succession & Nomination Rules

Buying luxury apartments is about building generational wealth. Ensuring that wealth passes to the right person requires clarity on succession.

Nominee vs. Legal Heir

This is a common misconception in India.

- Nominee: A nominee (e.g., in a cooperative society) is merely a trustee or caretaker of the property upon the owner’s death. They do not automatically become the owner.

- Legal Heir: The actual ownership passes to legal heirs as per the Will or personal succession laws.

The Importance of a Will

In “Tenancy-in-Common,” if a co-owner dies without a Will (intestate), their share gets distributed among all Class I heirs (spouse, children, and mother). This can complicate matters if the surviving co-owner (e.g., a brother) suddenly finds himself owning the house alongside his deceased brother’s wife and children.

- Solution: Always execute a Will clarifying who inherits your share of the joint property.

Why Location Matters: The Kondapur Advantage

When investing jointly, the asset quality matters as much as the legal structure. West Hyderabad, particularly Kondapur, has emerged as the preferred destination for joint investors.

Why Kondapur?

- Rental Yields: High demand from IT professionals ensures that flats for sale in Kondapur fetch premium rents, helping co-owners cover a significant chunk of their EMI.

- Appreciation: With the saturation of Hitec City, Kondapur is the immediate spillover zone. Investing in 3 BHK flats in Hyderabad‘s growth corridors ensures the asset value grows faster than inflation, protecting both partners’ capital.

Smart Ownership for a Secure Future

Joint home ownership is a powerful tool to fast-track your entry into the premium real estate market. It allows you to buy bigger, save more tax, and build a stronger asset base. However, it binds you legally and financially to another person.

The key to a successful joint purchase lies in transparency: clearly defined shares in the sale deed, a mutual understanding of financial contributions, and a rock-solid succession plan.

Ready to Make Your Joint Investment? Explore Auro Realty’s premium portfolio. Whether you are looking for investment-grade luxury apartments or a family home in Kondapur, our legal and sales experts can guide you through a seamless joint ownership process.

Sources & Legal Disclaimer

Legal provisions referenced in this guide are based on the Transfer of Property Act, 1882, Indian Registration Act, 1908, and Income Tax Act, 1961, as well as RERA Telangana guidelines (rera.telangana.gov.in). Registration procedures follow IGRS Telangana protocols (registration.telangana.gov.in).

Disclaimer: This article provides general legal and tax information for educational purposes. It does not constitute legal or tax advice. Please consult a qualified advocate or Chartered Accountant for guidance specific to your situation.

Frequently Asked Questions

What are the legal implications of joint home ownership in Hyderabad?

Joint home ownership in Hyderabad involves shared property rights, and all co-owners must be listed on the sale deed. Each owner has equal right to use and occupy the property unless otherwise agreed in a legal contract.

What are the tax benefits of joint home ownership in India?

Joint owners who are also co-borrowers can each claim individual tax deductions on home loan interest under Section 24(b) and principal repayment under Section 80C, effectively doubling the available tax benefits.

Can joint property owners sell their share independently in Hyderabad?

A joint owner can sell their undivided share of a property, but they cannot sell the specific portion without the consent of other co-owners. It is advisable to have a clear partition deed or joint ownership agreement.