At a Glance — What This Guide Covers

- The “Old vs. New” Regime Dilemma: Where Do Homeowners Stand?

- Latest Income Tax Deductions on Home Loans (FY 2025–26)

- Tax Benefits: First-Time Homebuyers vs. Repeat Buyers

- Tax Treatment: Under-Construction vs. Ready-to-Move Properties

- The “Double Dip”: How Joint Home Loans Impact Tax Savings

- Capital Gains Tax Rules on Property Sale & Reinvestment

- Smart Planning for Your Dream Home

Buying a home is more than just an emotional milestone; it is one of the smartest financial moves you can make. The home loan tax benefits available under India’s Income Tax Act can significantly reduce your financial burden, turning your EMI commitments into substantial annual tax savings.

As we navigate Financial Year 2025-26, the real estate landscape is booming, especially in high-growth corridors like Hyderabad. Whether you are eyeing premium residential projects in Hitec City or spacious 3 BHK flats for sale in Hyderabad, understanding the tax implications of your purchase is as important as checking the Vastu.

However, tax laws are not static. With the government pushing the New Tax Regime as the default option, many homebuyers are left asking: “Do I still get tax breaks on my home loan?”

This comprehensive guide decodes the complex jargon of Sections 80C, 24(b), and 54, helping you navigate the “Old vs. New” regime dilemma and ensuring you don’t leave any money on the table this assessment year.

For the Financial Year 2025-26, Indian homebuyers can save tax under the Old Tax Regime through the following sections:

- Section 24(b): Deduction of up to ₹2 Lakhs on home loan interest for self-occupied properties. (Unlimited for let-out properties).

- Section 80C: Deduction of up to ₹1.5 Lakhs on principal repayment (inclusive of stamp duty and registration charges).

- Joint Home Loan: Co-borrowers can claim these deductions separately, potentially doubling the total tax benefit to ₹7 Lakhs per household (₹3.5L x 2).

- Section 54: Exemption on Long-Term Capital Gains (LTCG) if reinvested in a new residential property (capped at ₹10 Crores).

- Note: Home loan tax benefits for self-occupied properties are generally not available under the default New Tax Regime.

Our Take: What Hyderabad Buyers Often Miss About Tax Benefits

Working with hundreds of first-time home buyers in Hyderabad, our team consistently finds that most buyers underutilize available tax benefits by 30-40%. The most common oversight? Not claiming the additional ₹1.5 lakh deduction under Section 80EEA for affordable housing, and missing the joint ownership strategy that effectively doubles deduction limits for working couples.

We’ve also seen confusion around the pre-construction interest deduction (Section 24b) — many buyers purchasing under-construction apartments in areas like Gachibowli and Narsingi don’t realize they can claim up to 5 years of pre-EMI interest in equal installments after possession. For a typical ₹80L apartment with a 2-year construction period, this translates to an additional ₹2-3 lakh in deductions that most buyers leave on the table.

— Auro Realty Team | Source: Income Tax Department, RBI Housing Finance Circulars

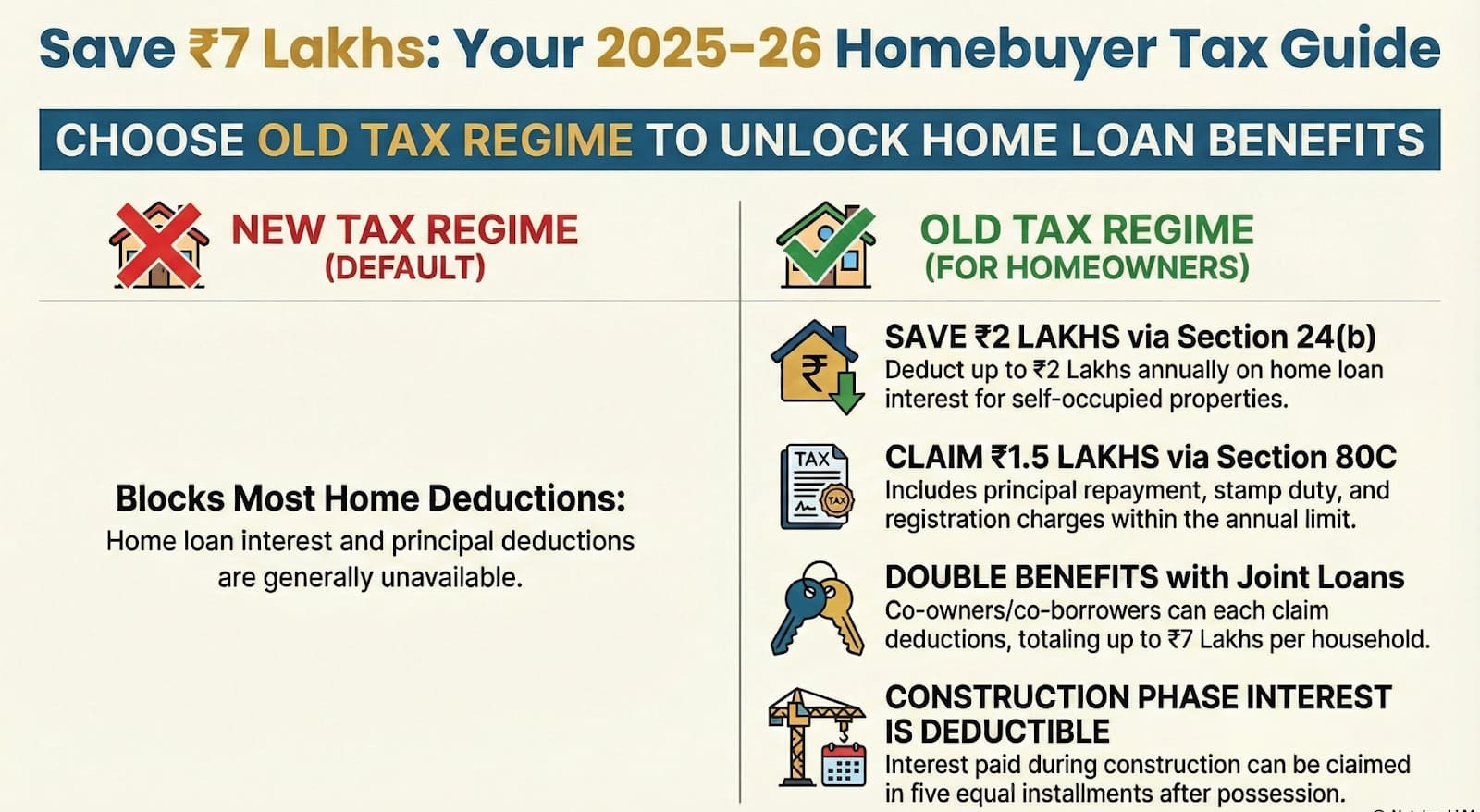

The “Old vs. New” Regime Dilemma: Where Do Homeowners Stand?

Before we list the deductions, we must address the most critical decision for FY 2025-26: Choosing your tax regime.

The New Tax Regime (Default)

The New Tax Regime offers lower tax slab rates but strips away most exemptions and deductions.

- The Bad News: You cannot claim deductions for home loan interest (Section 24b) or principal repayment (Section 80C) for a self-occupied property under this regime.

- The Exception: If you have let out (rented) the property, you can still claim interest deduction restricted to the rental income received.

The Old Tax Regime

- The Good News: This regime retains all the classic deductions. If you have a home loan, HRA, and insurance policies, the Old Regime usually results in lower tax liability.

- Strategy: Most homebuyers with a significant loan amount (e.g., those buying luxury apartments where interest exceeds ₹2 Lakhs) find the Old Tax Regime far more beneficial.

Latest Income Tax Deductions on Home Loans (FY 2025–26)

If you opt for the Old Tax Regime, your home loan acts as a powerful tax shield. Here is the breakdown of the sections you need to know.

A. Interest Payment Deduction: Section 24(b)

The interest component of your EMI is often the largest part of your repayment in the early years.

- Self-Occupied Property: You can claim a deduction of up to ₹2 Lakhs per financial year.

- Let-Out (Rented) Property: There is no upper limit on the interest you can deduct. However, if the loss from house property (Interest > Rent) exceeds ₹2 Lakhs, the remaining loss can be carried forward for 8 assessment years.

- Conditions:

- The loan must be for purchase or construction.

- The acquisition/construction must be completed within 5 years from the end of the financial year in which the loan was taken.

B. Principal Repayment Deduction: Section 80C

The principal component of your EMI falls under the crowded umbrella of Section 80C.

- Limit: ₹1.5 Lakhs per financial year.

- The Catch: This limit is shared with other investments like PPF, EPF, LIC premiums, and ELSS. If you are a salaried employee with a high PF contribution, this bucket might already be full.

- Lock-in Period: You must not sell the house within 5 years of possession. If you do, the deductions claimed in previous years will be added back to your income and taxed in the year of sale.

C. Stamp Duty and Registration Charges (Section 80C)

Did you know the hefty stamp duty fee is also deductible?

- These charges can be claimed under Section 80C (within the ₹1.5 Lakh limit).

- Crucial Rule: You can only claim this in the specific year the expenses were incurred. You cannot carry it forward to subsequent years.

D. Additional Interest Deduction: Section 80EEA (Status Check)

- Note for FY 2025-26: Section 80EEA, which offered an additional ₹1.5 Lakh deduction for affordable housing, had a sunset clause for loans sanctioned up to March 31, 2022. Unless re-introduced in a new budget, new borrowers in 2025 cannot claim this. However, existing borrowers who meet the criteria can continue to claim it until the loan is repaid.

Tax Benefits: First-Time Homebuyers vs. Repeat Buyers

The tax code treats you slightly differently depending on whether you are buying your first nest or building a portfolio of residential projects.

First-Time Homebuyers

First-time buyers traditionally enjoy more perks to encourage homeownership.

- 80EEA Legacy: If you sanctioned your loan before March 2022, you enjoy a total interest deduction of ₹3.5 Lakhs (₹2L under 24b + ₹1.5L under 80EEA).

- Current Scenario: Without 80EEA for new loans, first-time buyers are on par with repeat buyers regarding deduction limits (₹2L Interest + ₹1.5L Principal).

Repeat Buyers (Second Home)

Investing in a second property (e.g., a vacation home or an investment unit in luxury apartments)?

- Self-Occupied Second Home: As per recent amendments, you can declare two houses as “Self-Occupied.” However, the aggregate interest deduction for both houses combined is capped at ₹2 Lakhs.

- Deemed Let-Out: If you own more than two houses, the others are deemed to be let out, and you must pay tax on “notional rent” (the rent it could fetch), even if it’s vacant. This makes it crucial to actually rent out investment properties to offset the tax with actual income.

Tax Treatment: Under-Construction vs. Ready-to-Move Properties

This is a critical decision point for buyers of 3 BHK flats for sale in Hyderabad. Should you buy a ready home or invest in an upcoming project?

Ready-to-Move Properties

- Immediate Benefit: You can start claiming Section 24(b) and Section 80C deductions from the very financial year you take possession.

Under-Construction Properties

- The Restriction: You cannot claim tax deductions on EMIs paid while the property is under construction.

- Pre-Construction Interest (PCI): The interest paid during the construction phase is not lost. It accumulates and can be claimed in 5 equal annual installments starting from the year you receive possession.

- Limit: The total deduction (Current Year Interest + 1/5th of Pre-Construction Interest) is still subject to the overall cap of ₹2 Lakhs.

Pro Tip: If you buy a property with a long construction window, you lose out on the Section 80C principal deduction for those years entirely. This is why many tax-conscious buyers prefer residential projects nearing completion.

The “Double Dip”: How Joint Home Loans Impact Tax Savings

With property prices in premium locations rising, a single borrower’s tax limit often falls short. For example, a ₹1 Crore loan at 8.5% interest incurs ~₹8.5 Lakhs interest in the first year. A single applicant can only claim ₹2 Lakhs, leaving ₹6.5 Lakhs taxable.

The Solution: Joint Ownership + Joint Borrowing

If you buy the property jointly (e.g., with a spouse) and both serve the loan:

- Double Interest Benefit: Both can claim ₹2 Lakhs each u/s 24(b). Total = ₹4 Lakhs.

- Double Principal Benefit: Both can claim ₹1.5 Lakhs each u/s 80C. Total = ₹3 Lakhs.

- Total Tax Shield: A family can save tax on ₹7 Lakhs of income annually.

Requirements:

- Both must be co-owners of the property.

- Both must be co-borrowers in the loan.

- Both must contribute to the EMI payments.

Capital Gains Tax Rules on Property Sale & Reinvestment

If you are selling an old asset to upgrade to luxury apartments, you need to manage your Capital Gains Tax (CGT).

Long-Term Capital Gains (LTCG)

- Definition: Property held for more than 24 months (reduced from 36 months).

- Tax Rate: 12.5% without indexation (Union Budget 2024, effective July 23, 2024). The earlier option of 20% with indexation has been removed for properties sold on or after July 23, 2024. Properties acquired and disposed of before this date may still qualify for the 20% with indexation route. Always confirm with a CA for your specific situation.

Saving Taxes via Reinvestment (Section 54)

You can claim a 100% exemption on LTCG if:

- Reinvestment: You use the capital gains amount to buy/construct a new residential house in India.

- Timeline: Purchase within 1 year before or 2 years after the sale (or construct within 3 years).

- Cap: The maximum deduction under Section 54 is capped at ₹10 Crores. This specifically impacts Ultra High Net Worth Individuals (UHNIs) buying super-luxury homes.

Smart Planning for Your Dream Home

While the primary motive for buying a home should always be lifestyle and security, the tax benefits act as a significant subsidy on your purchase cost. By strategically choosing the Old Tax Regime, opting for a joint loan, and timing your possession, you can save substantial amounts—money that can be reinvested into furnishing your new home.

Whether you are looking for investment-grade residential projects or a family home, Hyderabad offers some of the best inventory in the country.

Ready to make a tax-efficient investment? Explore our collection of premium 3 BHK flats for sale in Hyderabad. From tax-friendly payment plans to properties nearing possession, Auro Realty helps you maximize value at every step.

Action Steps: Maximizing Your Tax Benefits

Before Buying:

- Calculate tax savings under both regimes using your actual salary and deductions.

- For loans above ₹50 lakhs, consider joint ownership to double benefits.

- Factor tax savings into affordability calculations—they effectively reduce borrowing costs.

During Purchase:

- Claim stamp duty/registration under Section 80C in the payment year.

- Maintain all loan-related documents (sanction letter, interest certificates, possession certificate).

Post-Possession:

- Opt for the Old Tax Regime when filing returns.

- Ensure both co-borrowers claim deductions separately if joint loan.

- Aggregate pre-construction interest for 5-year claim period.

Why Hyderabad Properties Offer Tax-Efficient Investment Opportunities

Hyderabads real estate market provides unique advantages. Property prices in corridors like Kondapur (₹8,000-12,000/sq ft), Gachibowli (₹10,000-15,000/sq ft), and Hitec City remain competitive versus Mumbai (₹25,000+/sq ft) or Bangalore (₹15,000+/sq ft), yet appreciation rates match or exceed these metros at 15-22% over 3-5 years.

The Sweet Spot: By utilizing joint home loans, dual-income couples can comfortably service EMIs for premium residential projects while maximizing tax deductions. The savings effectively subsidize the difference between standard apartments and luxury offerings with superior amenities, security, and resale value.

Turn Your Home Loan Into a Tax-Saving Asset

Tax planning shouldnt be an afterthought—its integral to smart home buying. By choosing the Old Tax Regime, leveraging joint ownership, and understanding possession timelines, you transform your home loan from a liability into a wealth-building, tax-efficient asset. The difference between knowing these provisions and ignoring them can amount to ₹10-15 lakhs over a typical 20-year loan tenure.

Frequently Asked Questions

What tax deductions can homebuyers claim in India for FY 2025-26?

Homebuyers can claim deductions on home loan interest up to Rs 2 lakh under Section 24(b), principal repayment up to Rs 1.5 lakh under Section 80C, and an additional Rs 50,000 under Section 80EEA for first-time buyers meeting specific criteria.

Can I claim tax benefits on both home loan principal and interest?

Yes, principal repayment qualifies under Section 80C (up to Rs 1.5 lakh) and interest payment qualifies under Section 24(b) (up to Rs 2 lakh for self-occupied property). Both deductions can be claimed simultaneously.

Are stamp duty and registration charges tax deductible for homebuyers?

Yes, stamp duty and registration charges paid during property purchase are deductible under Section 80C, subject to the overall limit of Rs 1.5 lakh. This deduction can be claimed in the year these expenses are paid.