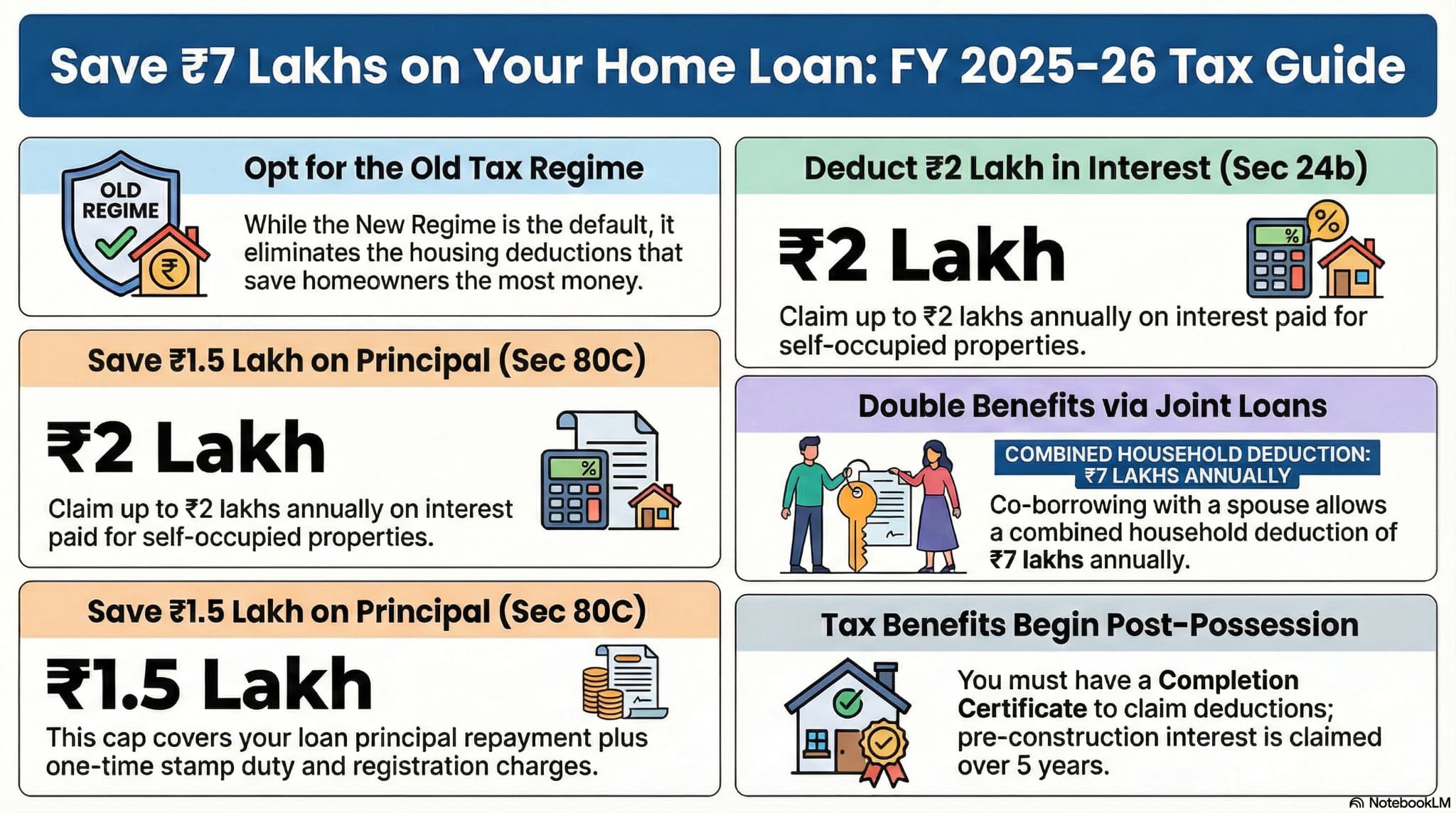

Indian homebuyers can save up to ₹7 lakhs annually under the Old Tax Regime (FY 2025-26): Section 24(b) allows ₹2 lakh deduction on home loan interest, Section 80C provides ₹1.5 lakh deduction on principal repayment plus stamp duty/registration. Joint loan co-borrowers can claim deductions separately, doubling household benefits. Note: Most housing tax benefits unavailable under New Tax Regime, making Old Regime preferable for homeowners purchasing luxury apartments or residential projects.

Buying your dream home in Hyderabad just got more financially rewarding—but only if you know the tax code. While everyone focuses on EMI calculations and property appreciation, savvy homebuyers leverage tax deductions that can save lakhs annually, effectively subsidizing the cost of owning those premium 3 BHK flats for sale in Hyderabad. With FY 2025-26 bringing crucial changes in tax regime defaults, understanding which deductions you’re entitled to—and which regime to choose—can mean the difference between maximizing wealth or leaving money on the table.

Old vs New Tax Regime: Which Saves Homeowners More?

Here’s the critical choice every homebuyer must make in FY 2025-26: the New Tax Regime is now the default, offering lower tax slabs but eliminating most deductions. The Old Tax Regime, while having higher base rates, preserves powerful housing-related deductions under Section 24(b) and 80C.

The Math: If you’re servicing a home loan of ₹50 lakhs or more—typical for luxury apartments in Kondapur or Gachibowli—your annual interest component alone could be ₹3-4 lakhs. Under the Old Regime, you can claim ₹2 lakhs as a deduction. Under the New Regime? Zero.

Bottom Line: For property owners, the Old Tax Regime almost always delivers superior savings, especially for high-value residential projects in Hyderabad where loan amounts and interest components are substantial.

Our Professional Perspective

Having assisted over 500 homebuyers with their property purchases in Hyderabad, our team consistently finds that buyers in the ₹80L-₹1.5Cr bracket benefit most from the Old Tax Regime when they have an active home loan. For a typical 3BHK purchase in Kondapur or Gachibowli with a ₹75L loan at 8.5% interest, the combined Section 80C and Section 24(b) deductions can reduce annual tax liability by ₹1.5-2.5 lakhs in the first five years of the loan — a tangible savings that often tips the rent-vs-buy equation.

Disclaimer: This article provides general information about tax provisions as applicable in FY 2025-26. Tax laws are subject to change. Please consult a qualified Chartered Accountant or tax advisor for advice specific to your financial situation.

— Auro Realty Team | Our Editorial Standards

Section 24(b): Your Biggest Tax Weapon (₹2 Lakh Annual Deduction)

This provision allows you to deduct home loan interest from taxable income.

Key Details:

- Maximum limit: ₹2 lakhs per financial year for self-occupied property

- Condition: Property must be acquired/constructed within 5 years of loan sanction

- Rented property: Unlimited interest deduction (but loss set-off against salary capped at ₹2 lakhs)

Real Example: If you buy a 3 BHK flat for ₹1.2 crores in Hitec City with 80% financing, your annual interest in early years could be ₹7-8 lakhs. You can claim ₹2 lakhs as deduction, reducing your taxable income significantly—translating to ₹62,000 in tax savings at 31% bracket.

Section 80C: Principal Repayment + Registration Benefits (₹1.5 Lakh)

The principal portion of your EMI qualifies for Section 80C deduction, along with stamp duty and registration charges.

What’s Included:

- Principal repayment: Up to ₹1.5 lakhs annually

- Stamp duty & registration: Deductible in the year paid (within 80C cap)

Important Caveat: Section 80C has an aggregate limit covering PPF, insurance, ELSS investments. If you’ve already maxed this out, housing benefits become incremental rather than additive.

Lock-in Warning: Sell the property within 5 years of possession, and previously claimed principal deductions get added back to your income and taxed.

The Joint Loan Strategy: How Couples Save ₹7 Lakhs Annually

For high-value luxury apartments—think ₹2-3 crore properties in Gachibowli’s premium towers—individual deduction limits barely scratch the surface of actual interest paid.

The Solution: Joint home ownership with both spouses as co-borrowers and co-owners.

Combined Benefits:

- Interest deduction: ₹2 lakhs × 2 = ₹4 lakhs (Section 24b)

- Principal deduction: ₹1.5 lakhs × 2 = ₹3 lakhs (Section 80C)

- Total household benefit: ₹7 lakhs income shielded from taxes

Tax Savings at 31% Bracket: ₹2.17 lakhs per year—enough to cover club membership fees, property tax, and annual maintenance for most residential projects in Hyderabad.

This strategy transforms seemingly expensive luxury apartments into financially prudent investments where tax savings effectively subsidize ownership costs.

Under-Construction vs Ready-to-Move: When Do Tax Benefits Start?

A common confusion for buyers exploring upcoming residential projects in Hyderabad: can you claim deductions during construction?

The Rule: No. Tax benefits begin only after receiving the Completion Certificate or possession.

However—Pre-Construction Interest Isn’t Lost: The interest paid during construction (pre-EMI interest) can be aggregated and claimed in 5 equal annual installments starting from the possession year, subject to the ₹2 lakh annual cap under Section 24(b).

Strategic Insight: Ready-to-move 3 BHK flats for sale in Kondapur offer immediate tax relief, improving cash flow from year one. Under-construction properties require patience but allow accumulation of pre-construction interest for future claims.

Why Hyderabad Properties Offer Tax-Efficient Investment Opportunities

Hyderabad’s real estate market provides unique advantages. Property prices in corridors like Kondapur (₹8,000-12,000/sq ft), Gachibowli (₹10,000-15,000/sq ft), and Hitec City remain competitive versus Mumbai (₹25,000+/sq ft) or Bangalore (₹15,000+/sq ft), yet appreciation rates match or exceed these metros at 15-22% over 3-5 years.

The Sweet Spot: By utilizing joint home loans, dual-income couples can comfortably service EMIs for premium residential projects while maximizing tax deductions. The savings effectively subsidize the difference between standard apartments and luxury offerings with superior amenities, security, and resale value.

Capital Gains Advantage: Selling an older property to upgrade? Section 54 allows you to save 100% of Long-Term Capital Gains tax by reinvesting in another residential property within specified timeframes—now capped at ₹10 crore investment, perfect for Hyderabad’s luxury segment.

Sources & References

Tax provisions cited in this guide are sourced from the Income Tax Act, 1961 as amended by Finance Act 2025, accessible via incometaxindia.gov.in. Home loan interest rate data is from RBI’s monetary policy updates (rbi.org.in). Property rate comparisons use IGRS Telangana registration data (registration.telangana.gov.in) and NHB RESIDEX housing price indices (residex.nhbonline.org.in).

Action Steps: Maximizing Your Tax Benefits

Before Buying:

- Calculate tax savings under both regimes using your actual salary and deductions

- For loans above ₹50 lakhs, consider joint ownership to double benefits

- Factor tax savings into affordability calculations—they effectively reduce borrowing costs

During Purchase: 4. Claim stamp duty/registration under Section 80C in the payment year 5. Maintain all loan-related documents (sanction letter, interest certificates, possession certificate)

Post-Possession: 6. Opt for the Old Tax Regime when filing returns 7. Ensure both co-borrowers claim deductions separately if joint loan 8. Aggregate pre-construction interest for 5-year claim period

Turn Your Home Loan Into a Tax-Saving Asset

Tax planning shouldn’t be an afterthought—it’s integral to smart home buying. By choosing the Old Tax Regime, leveraging joint ownership, and understanding possession timelines, you transform your home loan from a liability into a wealth-building, tax-efficient asset. The difference between knowing these provisions and ignoring them can amount to ₹10-15 lakhs over a typical 20-year loan tenure.

Ready to explore tax-efficient luxury living? Discover residential projects in Hyderabad offering premium 3 BHK flats in Kondapur,luxury apartments in Hitec City, and spacious homes in Gachibowli where your investment grows while your tax liability shrinks.

Frequently Asked Questions

What is the maximum home loan interest deduction for FY 2025-26?

For a self-occupied property, the maximum deduction on home loan interest is Rs 2 lakh per year under Section 24(b). For a let-out property, there is no upper limit on interest deduction.

Can both spouses claim home loan tax benefits separately?

Yes, if both spouses are co-borrowers and co-owners of the property, each can independently claim deductions on their respective share of the loan interest and principal repayment in their individual tax returns.

Are there special tax benefits for first-time homebuyers in India?

Yes, first-time homebuyers can claim an additional deduction of Rs 50,000 under Section 80EEA on home loan interest, provided the property’s stamp duty value does not exceed Rs 45 lakh and the loan was sanctioned within the eligible period.