Kondapur has rapidly evolved from a quiet suburb into one of Hyderabad’s most coveted residential zip codes. Nestled right next to the HITEC City IT corridor and Gachibowli’s financial district, it is the top choice for tech professionals and families seeking a “walk-to-work” lifestyle. But with property prices in West Hyderabad appreciating significantly, financing your dream home often requires a well-planned home loan strategy.

Navigating the mortgage landscape can feel overwhelming, especially for first-time homebuyers. Whether you are eyeing a luxury high-rise or a gated community apartment, securing a home loan for a Kondapur property doesn’t have to be complicated. This guide breaks down the entire process—from checking your eligibility to handing over the cheque to your builder—ensuring you get the best deal possible in 2026.

How to Apply for a Home Loan in Kondapur (2026 Guide)

To apply for a home loan in Kondapur, Hyderabad, follow these 5 steps:

- Check Home Loan Eligibility for Kondapur Properties: Ensure a credit score of 750+ and a debt-to-income ratio under 50%.

- Shortlist Lenders: Compare rates from top banks like SBI, HDFC, and ICICI (starting @ ~8.50%).

- Gather Documents: Prepare KYC proofs, 6 months’ bank statements, salary slips, and property builder NOCs.

- Submit Application: Apply online or visit a branch with the property’s sale agreement.

- Legal & Technical Verification: The bank will verify the property title and value before disbursing the loan.

Buying in Kondapur offers high rental yields (4-6%) and rapid appreciation due to HITEC City proximity.

Why Kondapur is the Smartest Real Estate Bet in 2026

Before diving into the paperwork, it is crucial to understand why banks are so willing to lend for properties in this area. Lenders view Kondapur as a “low-risk” zone. Why?

- High Liquidity: Kondapur Hyderabad flats for sale are in high demand, meaning the asset is easy to sell or rent out.

- Rental Yields: The area commands some of the highest rental yields in Hyderabad (averaging 4-5%), assuring banks that investors have a steady secondary income source to pay off EMIs.

- Infrastructure: With the proximity to the Metro, ORR, and top schools, property values here are shielded from market volatility.

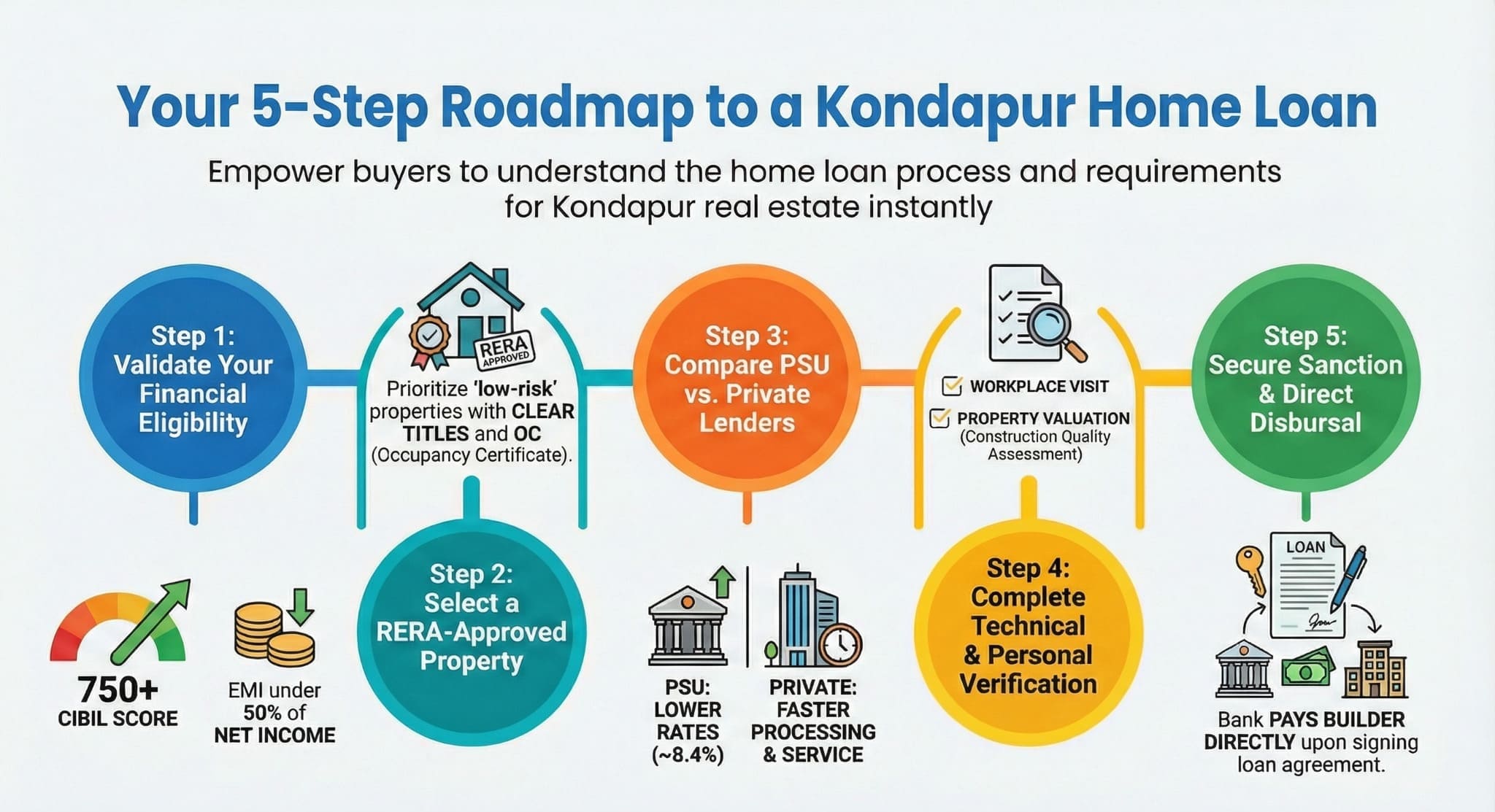

Step-by-Step Guide: How to Apply for a Home Loan in Hyderabad

Applying for a home loan for flats in Kondapur involves a systematic process. Follow these five steps to ensure hassle-free approval.

Step 1: Assess Your Financial Eligibility

Before falling in love with a property, know your budget. Use an EMI calculator for Hyderabad real estate to determine how much you can afford.

- The 50% Rule: Most banks prefer that your total EMIs (including the new home loan) do not exceed 50% of your net monthly income.

- Credit Score: A CIBIL score of 750 or above unlocks the lowest interest rates. Scores below 650 may lead to rejection or higher rates.

Step 2: Property Selection & Legal Check

Banks will not fund a property with unclear titles. When buying flats near HITEC City, ensure the project is RERA-approved. For resale properties, check for an Occupancy Certificate (OC).

- Note: Buying from a reputed developer like Auro Realty simplifies this step, as top-tier projects are often pre-approved by major banks, skipping the lengthy legal verification process.

Step 3: Compare Lenders & Interest Rates

Don’t settle for the first offer. Compare home loan interest rates in Hyderabad across:

- Public Sector Banks (SBI, Union Bank): Lower interest rates (approx. 8.4% – 8.65%) but stricter paperwork.

- Private Banks (HDFC, ICICI, Axis): Faster processing, better customer service, and slightly higher rates.

- NBFCs (Bajaj Finserv, LIC HFL): More lenient on credit scores but often carry higher interest rates.

Step 4: Submission & Verification

Once you submit your application, the bank initiates two checks:

- Personal Verification: They may visit your office or home to verify your employment and residence.

- Technical Verification: A bank-appointed valuator visits the property in Kondapur to assess its market value and construction quality.

Step 5: Sanction & Disbursal

If everything checks out, you receive a Sanction Letter. You will then sign the loan agreement, pay the processing fee, and the bank will disburse the amount directly to the builder or seller.

Eligibility Criteria for Home Loans in Telangana

To qualify for a home loan eligibility in Telangana, you generally need to meet the following criteria. Note that these can vary slightly between lenders.

| Criteria | Salaried Individuals | Self-Employed Professionals |

| Age Limit | 21 to 60 years | 21 to 65 years |

| Minimum Income | ₹25,000/month (Net) | ₹3 Lakhs/annum (Profit) |

| Work Experience | Min. 2 years total work exp. | Min. 3 years business continuity |

| CIBIL Score | 700+ (750+ preferred) | 700+ (750+ preferred) |

| Resident Status | Resident Indian / NRI | Resident Indian / NRI |

Documents Required for Home Loan in Hyderabad

Missing a single paper can delay your loan by weeks. Keep this checklist ready when applying for luxury apartments in West Hyderabad.

1. KYC Documents (All Applicants)

- Identity Proof: PAN Card (Mandatory), Aadhaar Card, Passport, or Voter ID.

- Address Proof: Utility bills (electricity/water), Rent Agreement, or Driving License.

- Passport Size Photos: 3-4 recent colored photographs.

2. Income Proof

- For Salaried:

– Last 3 months’ salary slips.

– Last 6 months’ bank account statements (salary account).

– Form 16 for the last 2 years.

- For Self-Employed:

– ITR (Income Tax Returns) for the last 3 years.

– Balance Sheet and P&L Account (CA audited).

– GST Registration certificate.

3. Property Documents (Crucial for Kondapur Properties)

- Sale Agreement: Copy of the agreement between you and the builder/seller.

- Title Deeds: Mother deed and link documents tracing ownership for the last 13-30 years.

- NOC from Builder: No Objection Certificate allowing you to mortgage the property.

- Encumbrance Certificate (EC): Proof that the property is free from legal dues.

- Occupancy Certificate (OC): Required if buying a ready-to-move Kondapur house for sale.

Top Banks for Home Loans in Hyderabad (2026 Overview)

Finding the best banks for home loans in Hyderabad depends on your priorities—lowest rate vs. fastest service.

- State Bank of India (SBI):

– Best for: Lowest interest rates and transparency.

– Pros: No hidden charges; interest calculated on a daily reducing balance.

– Cons: Slower processing time; strict documentation.

- HDFC Bank:

– Best for: Private sector efficiency and massive network in Kondapur.

– Pros: Rapid approvals; dedicated legal teams for property verification.

– Cons: Interest rates linked to RLLR (Repo Linked Loan Rate) can fluctuate.

- ICICI Bank:

– Best for: Pre-approved offers for existing customers.

– Pros: Minimal paperwork if you already hold a salary account.

– Cons: Processing fees can be higher compared to PSUs.

How to Improve Your Home Loan Approval Chances

Rejection can hurt your credit score. Use these tips to ensure your application for gated community apartments in Kondapur gets approved on the first try.

1. Clear Existing Debts

Banks calculate your Fixed Obligation to Income Ratio (FOIR). If you are already paying heavy EMIs for a car or personal loan, foreclose them before applying for a home loan to increase your eligibility.

2. Add a Co-Applicant

Adding a working spouse or parent as a co-applicant does two things:

- It combines your incomes, allowing you to borrow a higher loan amount.

- Women co-applicants often get a concession on interest rates (usually 0.05% lower).

3. Choose a Longer Tenure

Opting for a 25 or 30-year tenure reduces your monthly EMI, making you look less “risky” to the bank. You can always prepay the loan later when you have surplus funds (most floating-rate loans have zero prepayment penalties).

Making the Move to Kondapur

Buying a home is one of the biggest financial decisions you will make, and choosing the right location is half the battle won. Kondapur offers the perfect blend of cosmopolitan living, investment growth, and convenience. By securing a home loan with favorable terms, you aren’t just buying a flat; you are investing in a high-growth asset class that will pay dividends for decades.

Don’t let the paperwork daunt you. With clear titles, RERA approvals, and a robust credit score, your dream home in Kondapur is just a signature away.

Ready to find a home worth investing in?

Explore Auro Realty’s premium residential projects in Kondapur and HITEC City. We partner with leading banks to offer you seamless financing options for your dream home.

Frequently Asked Questions

What documents are needed to apply for a home loan in Kondapur?

Required documents include identity proof (Aadhaar, PAN), address proof, income proof (salary slips or ITR for self-employed), bank statements for 6 months, property documents, and builder approvals or sale agreement.

What is the typical home loan eligibility for buying property in Kondapur?

Most banks require a minimum monthly income of Rs 25,000-30,000, a credit score above 750, stable employment for at least 2 years, and the EMI should not exceed 40-50% of your monthly income.

Which banks offer the best home loan rates for properties in Kondapur?

SBI, HDFC, ICICI, and LIC Housing Finance are popular choices with competitive interest rates. Many builders in Kondapur have pre-approved project tie-ups with banks, which can simplify and speed up the loan process.